On Friday AAPL closed New York trading at $326.35, down $4.88 on the day. At that price Apple is trading at a price-earnings multiple of 15.55 times trailing 12-month earnings of $20.99 per share. This lowly valuation includes more than $70 per share in cash on Apple's balance sheet and is in the context of an earnings per share growth rate of 83.2% in the first six months of the current fiscal year.

On June 12th I published my updated 12-month price target for AAPL of $590 per share. At Friday's closing price of $326.35 a $590 target price might seem ambitious. It's an anticipated 80% rise in the share price in roughly 12 months. But as I will detail in this article, AAPL is trading not only at a low historical p/e multiple since the elimination of deferred revenue accounting on the iPhone in FQ1 2010, but is also trading significantly below the current price targets of the Wall Street pros.

AAPL: The Coiled Spring

For this article I asked Jeff Fosberg of the Apple Finance Board to update his popular "coiled spring" graphic to reflect Friday's closing prices for three popular publicly traded enterprises: Amazon, Apple and Netflix. The graphic compares the valuations of the three companies based on current price-earnings multiples and the gap between the current median price target from Wall Street analysts and Friday's closing prices.

I do not view price-earnings multiples as an effective means to compare companies in dissimilar industries. Amazon, Apple and Netflix do not compete directly in their respective core markets and Apple's hardware products are revenue conduits for products and services offered by Amazon and Netflix. The markets for the Amazon Kindle and the Apple iPad only partially overlap. However, comparing the gap between current trading prices and Wall Street price targets makes for a compelling contrast between the valuations of the three companies.

No matter the 82.3% rise in eps in the first six months of Apple's current fiscal year, the average estimate among analysts calls for eps in FY2011 (ending in late September) of $24.76 versus $15.15 in FY2010, a gain of 63.4% with less than six months remaining in the one-year period. For FY2012 the current average eps estimate of $28.72 represents only a 16% gain above the estimated current fiscal year eps performance.

Over the next five months inclusive of the release of Apple's FQ3 and FQ4 results, both the FY2011 and FY2012 analyst eps estimates and corresponding price targets will rise dramatically, providing strong catalysts for not only a share price recovery but also a continuing strong share price advance.

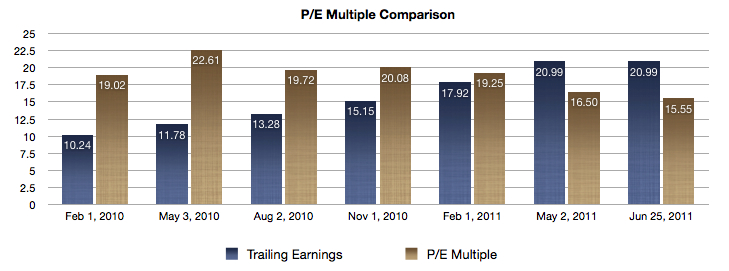

The Post-Deferred Revenue Era

From the launch of the original Apple iPhone in the summer of 2007 through the end of Apple's FY2009, the company reported iPhone revenue using a deferred revenue accounting principle due to the free OS upgrades offered to iPhone owners following purchase and the consequential revenue reporting requirements under Sarbanes-Oxley (SOX) that applied at the time.

Beginning with the release of FQ1 2010 results in January of that year, Apple eliminated virtually all elements of deferred revenue accounting for the iPhone and began reporting full revenue from iPhone handset sales in the quarter in which the sales were generated. This change renders share price performance comparisons with periods prior to that January date imprecise and prone to misinterpretation. For this reason the Apple share price valuations depicted in the graph below begin with the FQ1 2010 results.

Apple is currently trading at its lowest price-earnings multiple since the elimination of deferred revenue accounting on the iPhone and is currently valued at only 72.5% of the Wall Street analyst median price target of $450 per share. At Friday's closing price Apple is trading at 11.87 times my estimated FY2011 eps of $27.50 and 8.16 times my forecast FY2012 eps of $40 per share.

Conclusion

Even if today's comparatively low price-earnings multiple of 15.55 times trailing 12-month earnings remains a constant, earnings growth alone will propel the share price to over $425 by early November 2011, following the release of FQ4 2011 results. Earnings growth is the strong foundation for share price appreciation. Revisions to Wall Street earnings estimates and the resulting expansion in the median 12-month price target will also provide momentum for a dramatic move higher in the share price over the next six to twelve months. But just filling more of the gap between Friday's closing price of $326.35 and the current median price target of $450 provides room for a major share price advance.

Robert Paul Leitao

Disclosure: The author is long AAPL shares

Posts At Eventide Resource Guide

The objective of the Posts At Eventide web presence is to benefit readers seeking to understand Apple's financial performance and to serve as a repository of information and analysis for other independent AAPL analysts preparing quarterly estimates and share price forecasts. Please see the Posts At Eventide Resource Guide for more information.

No comments:

Post a Comment